[fusion_builder_container hundred_percent=”no” hundred_percent_height=”no” hundred_percent_height_scroll=”no” hundred_percent_height_center_content=”yes” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” status=”published” publish_date=”” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” enable_mobile=”no” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” video_preview_image=”” border_size=”” border_color=”” border_style=”solid” margin_top=”” margin_bottom=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=””][fusion_builder_row][fusion_builder_column type=”1_2″ layout=”1_2″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” border_radius=”” box_shadow=”no” dimension_box_shadow=”” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”” margin_bottom=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” last=”no”][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Intro:

Over the last five trading days TNXP’s price has enjoyed a notable parabolic run resulting in a three-fold increase. Daily trading volume has also picked up significantly, setting a new record level yesterday, with more 265 million shares traded. Given this somewhat common (in this day and age of “unorthodox” quantitative easing) market activity we decided to take a closer look at TNXP and unsurprisingly we found enough red flags to warrant putting out a short report. These red flags include: extreme levels of dilution that have worsened over the last few months; relatively recent paid promotion and the involvement of several funds with a less than outstanding track record.

[/fusion_text][/fusion_builder_column][fusion_builder_column type=”1_2″ layout=”1_2″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” border_radius=”” box_shadow=”no” dimension_box_shadow=”” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”” margin_bottom=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” last=”no”][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Security Details:

Symbol: TNXP

Current price: ~$2.07

Outstanding shares: 125.7 million

Market Cap: ~$260.2 million

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container][fusion_builder_container hundred_percent=”no” hundred_percent_height=”no” hundred_percent_height_scroll=”no” hundred_percent_height_center_content=”yes” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” status=”published” publish_date=”” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” enable_mobile=”no” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” video_preview_image=”” border_size=”” border_color=”” border_style=”solid” margin_top=”” margin_bottom=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=””][fusion_builder_row][fusion_builder_column type=”1_2″ layout=”1_2″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” border_radius=”” box_shadow=”no” dimension_box_shadow=”” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”” margin_bottom=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” last=”no”][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Company information:

Tonix Pharmaceuticals describes itself as a “clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing drugs and biologics to treat and prevent human disease and alleviate suffering”. Its current portfolio includes “biologics to prevent infectious diseases and small molecules and biologics to treat pain, psychiatric and addiction conditions”. According to a February 26 press release, TNXP is currently “collaborating with the Southern Research Institute, or Southern Research, to support the development of TNX-1800 (live modified horsepox virus vaccine for percutaneous administration), a potential vaccine to protect against COVID-19”. It thus appears that as countless other small cap biotechs, TNXP has jumped on the Covid-19 vaccine bandwagon in an attempt to raise the money it needs to stay afloat and service its financial obligations.

[/fusion_text][/fusion_builder_column][fusion_builder_column type=”1_2″ layout=”1_2″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” border_radius=”” box_shadow=”no” dimension_box_shadow=”” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”” margin_bottom=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” last=”no”][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Recent News:

- July 16, 2020, Tonix Pharmaceuticals Announces Research Collaboration to Develop Precision Medicine Techniques for COVID-19 Vaccines and Therapeutics

- July 15, 2020, Tonix Pharmaceuticals Holding Corp. Closes $10.5 Million Common Stock Registered Direct Offering

- July 13, 2020, Tonix Pharmaceuticals Holding Corp. Prices $10,500,000 Common Stock Offering

- July 12, 2020, TNXP: 50% Enrollment Reached in Phase 3 RELIEF Trial of TNX-102 SL in Fibromyalgia; Interim Analysis in Sep. 2020

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container][fusion_builder_container hundred_percent=”no” hundred_percent_height=”no” hundred_percent_height_scroll=”no” hundred_percent_height_center_content=”yes” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” status=”published” publish_date=”” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” enable_mobile=”no” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” video_preview_image=”” border_size=”” border_color=”” border_style=”solid” margin_top=”” margin_bottom=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=””][fusion_builder_row][fusion_builder_column type=”1_1″ layout=”1_1″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” border_radius=”” box_shadow=”no” dimension_box_shadow=”” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”” margin_bottom=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” last=”no”][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Financial Highlights:

[/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

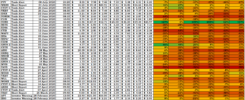

A quick glance at TNXP’s latest quarterly financials will show a relatively healthy clinical stage biopharmaceutical. On March 31, 2020, the company was sitting on over $30 million in cash and the average quarterly loss for 2019 was “only” around $7 million, meaning that the company should have enough cash to survive for the next few months. But this liquidity has come at a price for long time shareholders as the number of outstanding shares has ballooned over the last year, a trend that has accelerated in recent months, which in turn has resulted in extreme levels of dilution. This is evidenced by the fact that on June 30, 2019 the total number of TNXP outstanding shares stood at a mere 6,338,320, and now this number adds up to an astonishing 125 million, with nearly 21 million of these being issued through a recent registered direct offering amounting to $10.5 million at $0.50 a share. This is all the more shocking if one bears in mind that a 1-for-10 reverse split took place on November 1, 2019, meaning that dilution is a lot greater than it seems at first glance. Consequently, one TNXP share nowadays corresponds to around a twentieth of the equity it represented little over a year ago. It thus appears that TNXP’s management is not particularly concerned with long term shareholder value. The below table shows the monumental dilution long term TNXP shareholders have had to put up with:

[/fusion_text][fusion_imageframe image_id=”4085|full” max_width=”” style_type=”” blur=”” stylecolor=”” hover_type=”none” bordersize=”” bordercolor=”” borderradius=”” align=”center” lightbox=”no” gallery_id=”” lightbox_image=”” lightbox_image_id=”” alt=”” link=”” linktarget=”_self” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″]https://utopiacap.wordpress.com/wp-content/uploads/2024/07/453c9-tnxp2-dilution.png[/fusion_imageframe][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Furthermore, it appears that this trend is likely to continue as the company registered over $150 million worth of equity for sale in April this year, meaning that new shareholders can likely expect the dilution issues to continue for the foreseeable future.

[/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Paid promotion:

[/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

One of the biggest red flags TNXP raises is its use of paid promotion to tout its shares to prospective investors around the time it is conducting an offering. TNXP makes use of Zack’s Small Cap Research to publish paid for content. The most recent example we could find is a report that clearly states that Zacks Small Cap Research “received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm engaged by the issuer for providing non-investment banking services to this issuer and expects to receive additional compensation for such non-investment banking services provided to this issuer”. This compensation consists of an annual payment of $40,000.

[/fusion_text][fusion_imageframe image_id=”4087|full” max_width=”” style_type=”” blur=”” stylecolor=”” hover_type=”none” bordersize=”” bordercolor=”” borderradius=”” align=”center” lightbox=”no” gallery_id=”” lightbox_image=”” lightbox_image_id=”” alt=”” link=”” linktarget=”_self” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″]https://utopiacap.wordpress.com/wp-content/uploads/2024/07/983fa-tnxp2-zacks-promo.png[/fusion_imageframe][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Paid promotion is very worrying as it is an indication that the company’s fundamentals and prospects are not enough to entice potential investors.

[/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

The involvement of a few “opportunistic” investors:

Yet another big red flag TNXP raises is its involvement with several entities with very “interesting” track records.

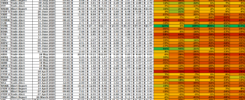

First up we have got Lincoln Park Capital, which we believe to be one of the most prolific so-called “vulture funds” currently operating among small caps, due to the rather remarkable (for all the wrong reasons) long term performance of the share price of the vast majority of public companies that it gets involved with. As stated on TNXP most recent prospectus supplement: “The sale or issuance of our common stock to Lincoln Park may cause dilution and the sale of the shares of common stock acquired by Lincoln Park, or the perception that such sales may occur, could cause the price of our common stock to fall. On September 28, 2017, we entered into the Purchase Agreement with Lincoln Park, pursuant to which Lincoln Park has committed to purchase up to $15,000,000 of our common stock. Upon the execution of the Purchase Agreement, we issued 73,039 shares of common stock to Lincoln Park as a fee for its commitment to purchase shares of our common stock under the Purchase Agreement. The remaining shares of our common stock that may be issued under the Purchase Agreement may be sold by us to Lincoln Park at our discretion from time to time through March 2020. The purchase price for the shares that we may sell to Lincoln Park under the Purchase Agreement will fluctuate based on the price of our common stock. Depending on market liquidity at the time, sales of such shares may cause the trading price of our common stock to fall”.

Another “interesting investor” TNXP has been involved with for a few years is Sabby Management. Sabby is another so-called “vulture fund” with an “impressive” track record when it comes to small caps, in addition it has settled with the SEC in the past for short selling rules violations. It appears that Sabby has been financing TNXP since early 2015 and according to the latest ownership form relating to TNXP, which was filed in mid February 2020, Sabby currently holds little over 1.2 million shares. These shares were acquired by Sabby around the same time the company announced the sale of millions of shares and warrants priced at around £0.57 each, meaning that if Sabby got hold of these shares, it stands to make substantial profits if they were to be sold at current market prices.

[/fusion_text][fusion_imageframe image_id=”4089|full” max_width=”” style_type=”” blur=”” stylecolor=”” hover_type=”none” bordersize=”” bordercolor=”” borderradius=”” align=”center” lightbox=”no” gallery_id=”” lightbox_image=”” lightbox_image_id=”” alt=”” link=”” linktarget=”_self” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″]https://utopiacap.wordpress.com/wp-content/uploads/2024/07/05e7d-tnxp2-sabby.png[/fusion_imageframe][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Yet another dubious institutional shareholder involved with TNXP is Iroquois Capital. According to an article published on August 16, 2018 by Teri Buhl, Richard K. Abbe, a co-founder of Iroquois Capital was accused of a fraudulent scheme to trick the founders of an airport spa business, XpresSpa, into a merger with a public Microcap company that resulted in a massive loss of their business investment. A federal judge in New York allowed a securities fraud case to go forward against Abbe and other company executives.

[/fusion_text][fusion_imageframe image_id=”4090|full” max_width=”” style_type=”” blur=”” stylecolor=”” hover_type=”none” bordersize=”” bordercolor=”” borderradius=”” align=”center” lightbox=”no” gallery_id=”” lightbox_image=”” lightbox_image_id=”” alt=”” link=”” linktarget=”_self” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″]https://utopiacap.wordpress.com/wp-content/uploads/2024/07/72592-tnxp2-iroquois-lawsuit.png[/fusion_imageframe][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

In addition, Aegis Capital entered into an underwriting agreement with TNXP on July 16, 2019, which allowed it to obtain a fair number of shares at discounted price meaning that they only paid $0.48 per share. Aegis is no stranger to SEC issues as they were subject to a cease and desist order in March, 2018 because it failed to file Suspicious Activity Reports (“SARs”) on hundreds of transactions when it knew, suspected, or had reason to suspect that the transactions involved the use of the broker-dealer to facilitate fraudulent activity or had no business or apparent lawful purpose. Many of the transactions involved red flags of potential market manipulation, including high trading volume in companies with little or no business activity during a time of simultaneous promotional activity.

[/fusion_text][fusion_imageframe image_id=”4091|full” max_width=”” style_type=”” blur=”” stylecolor=”” hover_type=”none” bordersize=”” bordercolor=”” borderradius=”” align=”center” lightbox=”no” gallery_id=”” lightbox_image=”” lightbox_image_id=”” alt=”” link=”” linktarget=”_self” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″]https://utopiacap.wordpress.com/wp-content/uploads/2024/07/c210d-tnxp2-aegis.png[/fusion_imageframe][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Red Flags:

[/fusion_text][fusion_imageframe image_id=”4092|full” max_width=”” style_type=”” blur=”” stylecolor=”” hover_type=”none” bordersize=”” bordercolor=”” borderradius=”” align=”none” lightbox=”no” gallery_id=”” lightbox_image=”” lightbox_image_id=”” alt=”” link=”” linktarget=”_self” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″]https://utopiacap.wordpress.com/wp-content/uploads/2024/07/9e8ee-tnxp-2-flags.png[/fusion_imageframe][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=””]

Opinion:

TNXP is a poor investment. It is a company that has been issuing very large numbers of shares at prices well below current market prices for many years, a worrying trend that has accelerated recently. This in turn has resulted in very high levels of dilution and explains why TNXP’s price has been steadily declining for years. Furthermore, many of the funds involved with the company have highly questionable track records when it comes to small caps and have acquired millions of cheap shares and are unlikely to hold to them for very long. Consequently, there is a very large supply of cheap shares out there. Furthermore, the company has employed the services of paid promoters to publish reports relating to its potential Covid 19 treatment vaccine recently, meaning that the company is trying to generate demand for its shares. This combination of an abundant supply of cheap shares (some of which are in the hands of funds with “interesting” track records), “artificial” share demand generation through paid promotion and a recent parabolic price run should greatly concern existing long term investors and any traders hoping for the run to continue. Stay away from TNXP unless you are an experienced trader.

[/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=””]

GET OUR LATEST REPORTS AND TRADE ALERTS DELIVERED TO YOUR INBOX

[/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=””][mailpoet_form id=”1″][/fusion_text][fusion_text columns=”” column_min_width=”” column_spacing=”” rule_style=”default” rule_size=”” rule_color=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=””]

Short seller Academy

Utopia Cap’s Short seller Academy is focused on the short side of trading. Through years of constant monitoring and trading of the American stock market, our members have acquired a wealth of knowledge that has allowed them to device various methods of shorting opportunity identification and trading. Our approach leans heavily on extensive due diligence and in-depth research and seeks to expose potential fraud and criminal activity, something we take great pride in. For More information on how to JOIN US -> Short seller Academy

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]